If you own a modified car, you probably need to modify your car insurance, too. This isn’t just true for hot rods and custom builds. It also goes for any car with significant non-factory standard parts.

This isn’t an exhaustive or exclusive list: Possible car modifications are endless. But here are some of the most common car modifications that can have an effect on your car insurance strategy:

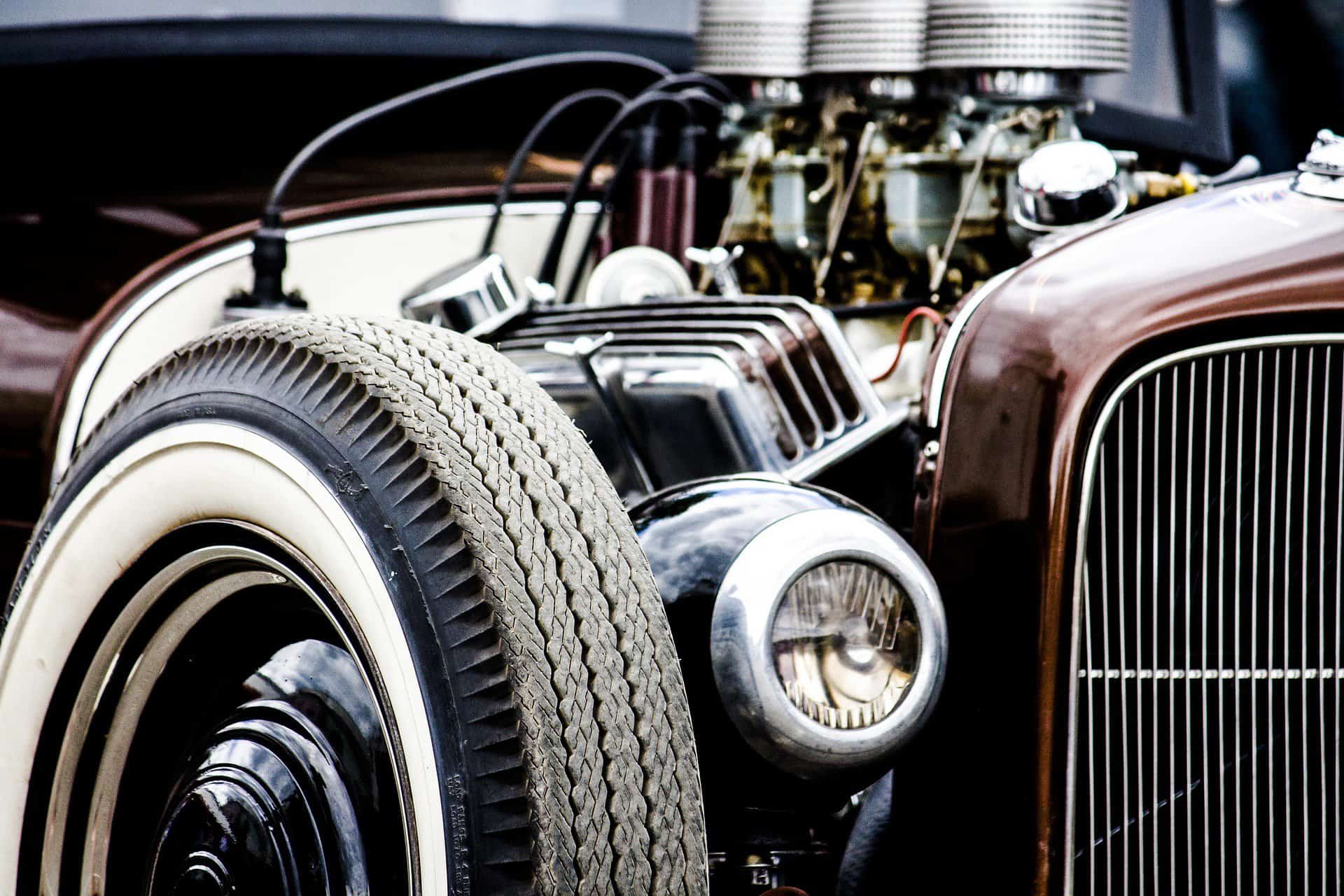

- Chrome rims or bumpers

- Swapped engines

- Turbochargers

- Strut/sway bars

- Custom paint jobs

- Lift kits and hydraulics

- Turbochargers or turbo boosters

- Stereo systems, subwoofers,

- CD or DVD players and entertainment systems

- Custom grilles and air intakes

- Foils and emblems

- Custom leather or suede interiors

- Restorations made with aftermarket or custom-made parts

- Those tiny little steering wheels made out of chain links

- Barbie, Hello Kitty, and other ‘theme’ work

Background.

Standard auto insurance policies are written and priced with the assumption that the vehicle has all original manufacturer parts. If the parts themselves are not the original to the vehicle, they are at least made by the car manufacture. Any deviations are minor issues that don’t materially affect the the value of the car.

Normie policies are not designed or priced to cover your all-chrome front grille, your larger-than-life space-age rims, your awesome hydraulics on your pristine white 1964 low rider Chevy Impala SS Coupe, the Pride of East L.A. (let’s go, Doyers!), or your gee-whiz Mopar 6.9 L 1.000HP V8 Hellephant engine you and your mates have somehow shoehorned into your 2018 Volkswagen Jetta.

If you and your baby get in a wreck with a normie, off-the-shelf car insurance policy from your golf buddy who sells homeowner, auto, and fire insurance from his office down at the strip mall. the best case scenario is that your insurance company will pay out the actual cash value of an unmodified car with nothing but factory parts, and the normal amount of wear and tear. Which will be much less than the replacement cost of your hot rod.

In the worst-case scenario, your carrier might not pay out at all, and may void or rescind the policy.

This is especially true if the car is stolen, or if thieves rip off the rims or other parts that you didn’t tell your insurance company were on the car.

Car insurance companies know how often each model of car gets stolen. If you have major conspicuous modifications on a car, that could increase the likelihood that thieves specifically target the car for its valuable parts.

That throws off the insurance company’s calculations. If you didn’t tell the carrier up front, you may have materially misrerepsented not just the value of the car, but the risk of theft or vandalism.

So in the hot rod and performance context, your car mods will almost certainly increase your insurance premiums.

Car Modifications that Lower Insurance Premiums

But car modifications don’t always cause insurance premiums to go up. Some modifications can actually help reduce your insurance premiums. For example, installing daytime running lamps, rear-view cameras, and modern anti-theft and car tracking devices, or telemetrics technology to standard cars helps lower the risk for insurance companies, and in turn helps you qualify for lower premiums.

With higher-end cars, some of these modifications can pay for themselves, over time, if you’re planning on keeping the car for years.

Insurance Considerations For Hot Rods, Muscle Cars, and Modified Cars

When you shop for insurance for your hot rod, restored, or modified car, you need to do things differently.

First, you’ll either need a special endorsement on your standard car insurance policy listing the added, custom, or aftermarket parts, along with their replacement value.

If the mods are extensive, it’s more likely you need a custom-designed insurance policy from a carrier that specializes in the hot rod world.

Agreed Value vs. Actual Cash Value

You should also look at getting an agreed value policy, rather than a standard, off-the-shelf, generic car insurance policy that the Muggles get.

Custom cars, collectibles, classics, exotic cars, and hot rods don’t depreciate over time the same way normie cars do. Sometimes, they even go up in value.

That changes the way you need to insure them.

Your run-of-the-mill, garden-variety, M1A1 one-each car insurance policy reimburses drivers for totaled cars based on the fully-depreciated value of the car. That is, they subtract for age, wear-and-tear, and mileage. The resulting number is called the actual cash value. And then they subtract the deductible from that, and that’s the most you’ll receive under the policy.

What’s more, over time, the depreciation would cause your protection to become more and more inadequate, as paper depreciation causes an ever-widening chasm between the car’s insured value and the actual market value of the car.

Such a policy would not come close to making you whole after a total loss via wreck, theft, natural disaster, or vandalism.

To insure one of these non-standard cars, you should look at getting an agreed value policy.

With these policies, you and the insurance company agree on a fair value for the car in advance. You may even build in increases over time to account for inflation and appreciation in the custom car market.

Get a Professional Custom Car Specialist Insurance Agent

Not every car insurance company will insure custom cars, mods, and hot rods. And even then, most won’t insure above a fixed dollar value on any single car. Some insurance companies just don’t understand the custom and hot rod market, and therefore don’t play in it. They don’t have an appetite for that type of risk, and they wouldn’t know how to price it if they did.

Furthermore, all car insurance agents are the same, either. Especially when it comes to specialty cars. Not every car insurance agent will know what to do with your application. Some folks just aren’t “car people.”

You also need a non-standard car insurance agent who understands hot rods and muscle cars. One who’s not an “order taker” drone working by the hour in a call center somewhere, but a professional agent who’s making a career out of car insurance, and who’s a car freak himself (or herself. They’re out there! If you know any, male, female, or whatever, I’m looking to hire some agents!)

A professional, experienced agent will know how to tailor your application, deal with the underwriters, and get your policy written up so it truly covers your risk.

It might cost a little more. But it’s worth it.

Got a hot rod? Custom job? Restoration? Barnyard beauty? Frankencar? Is your Nissan GTR the Queen of the Car Show? Does the valet service at your favorite downtown martini bar make room to park your car directly in front of the building near the street because your car “has eyes?”

We want to be your insurance company.

Here’s the page to contact us.

Don’t bother with the “get your free quote” thingie. It works great for normie cars. But if you’ve got one of those beautiful weirdos on your hands, you’ll need a custom-designed policy. So pick up the phone, dial 855-438-7353, and ask to speak to one of our car freak agents.

Looking forward to working with you, and I’ll see you on the road.

Steve “Mr. Insurance” Ludwig

CEO, Select Insurance Group

All-Around Car Guy

You Might Also Like:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}